In recent years, there has been concern among policymakers about increasing consolidation in the U.S. health care system. One particular concern is that consolidation of health systems and hospitals (including physician practice acquisition) has reduced competition, leading to higher prices and potentially reduced benefits for patients.

Indeed, the worry has grown sufficiently that in 2023, the Federal Trade Commission and the U.S. Department of Justice released draft merger guidelines for the health care sector, seeking to promote transparency for employers and consumers, strengthen antitrust enforcement, and initiate reimbursement reform.1 In addition, 36 bills regarding the consolidation of health systems — ranging from contractual affiliation notifications to certificate of need reviews — were enacted across 24 states in 2023.2 Federal proposals to create a new agency or task force to monitor, oversee, and intervene in health care markets have also been discussed.3 To further promote competition in health care markets, the U.S. Department of Health and Human Services recently named its first chief competition officer.4

- U.S. Department of Justice and U.S. Federal Trade Commission. 2023 Draft Merger Guidelines. Washington, DC: U.S. Department of Justice and U.S. Federal Trade Commission; 2023. https://www.justice.gov/d9/2023-12/2023%20Merger%20Guidelines.pdf. Back to text ↑

- Scotti S and Davenport K. 2023 Legislative Recap: Health Care Consolidation and Competition. National Conference of State Legislatures. https://www.ncsl.org/state-legislatures-news/details/2023-legislative-recap-health-care-consolidation-and-competition. Published Sept. 28, 2023. Accessed Nov. 28, 2023. Back to text ↑

- Dafny L. Addressing consolidation in health care markets. JAMA. 2021;325(10):927-928. doi:10.1001/jama.2021.0038. https://jamanetwork.com/journals/jama/fullarticle/2776037. Back to text ↑

- U.S. Department of Health and Human Services Press Office. Secretary Becerra names chief competition officer to help identify areas to promote competition in health care. Jan. 8, 2024. https://www.hhs.gov/about/news/2024/01/08/secretary-becerra-names-chief-competition-officer-to-help-identify-areas-to-promote-competition-in-health-care.html. Back to text ↑

Health systems argue that consolidation has been driven by financial pressures as well as opportunities to eliminate excess capacity, integrate care for patients, gain efficiencies, and improve leverage for negotiating with private insurers, among other reasons.5 Indeed, the extensive consolidation of the insurance industry has played a large role in dictating how health systems compete in the marketplace. This analysis seeks to examine and compare the market share of providers and insurers in order to show the implications of consolidation across the two industries.

- Medicare Payment Advisory Commission. Report to the Congress: Medicare Payment Policy. Washington DC: Medicare Payment Advisory Commission; 2020. https://www.medpac.gov/wp-content/uploads/import_data/scrape_files/docs/default-source/reports/mar20_entirereport_sec.pdf. Back to text ↑

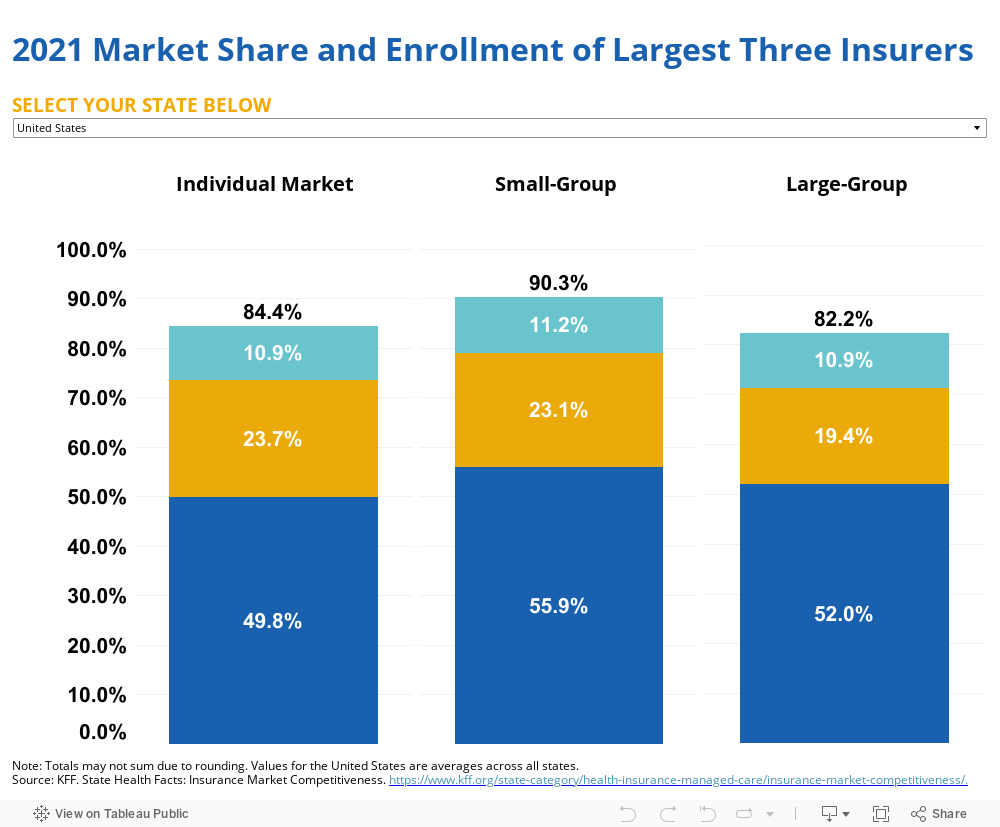

To shed light on the presence of market consolidation, we assessed the market share of each health system (defined as at least one hospital and at least one group of physicians providing comprehensive care connected with each other through common ownership or joint management) by looking at the health systems with the largest shares of inpatient hospital discharges in each state. We then compared those to the market share of the largest large-group insurers in each state as measured by enrollment.

While most critiques of health care consolidation have focused on hospitals within a metropolitan statistical area (MSA) and insurers at the national level, we suggest that states are a potentially useful unit of analysis given patient mobility, virtual care, and the fact that licensure and insurance are often regulated at the state level.

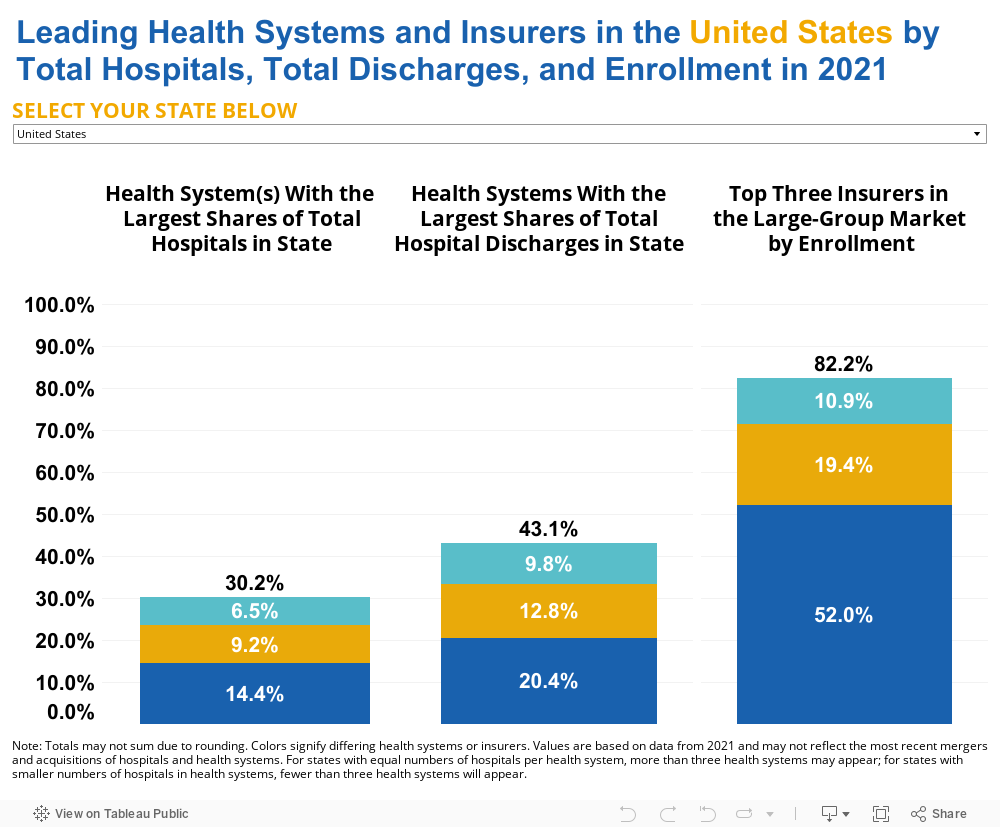

Overall, our data show that the largest health systems have, on average, a combined 43.1% of the market share (as measured by total inpatient hospital discharges) in each state, while the top three large-group insurers hold an average of 82.2% of the market share in each state. For instance, in North Carolina, the largest health systems — Atrium Health (20.3% of inpatient hospital discharges), University of North Carolina Health Care System (14.9%), and Novant Health (14.4%) — have a combined market share of 49.6% in the state. But the largest insurers — Blue Cross Blue Shield of North Carolina (74.9%), UnitedHealth Group (16.2%), and Cigna Health Group (4.4%) — have a combined 95.5% of the market share. Likewise, in Massachusetts, the largest health systems — Mass General Brigham (19.8% of inpatient hospital discharges), Beth Israel Lahey Health (19.5%), and Steward Health Care System (8.3%) — have a combined 47.6% of the market share in the state. But the largest insurers, those with the highest enrollment, in Massachusetts — Blue Cross Blue Shield of MA (60.7%), Point32Health, Inc. Group (23.5%), and UnitedHealth Group (4.2%) — have a combined 88.4% of the market share. Interestingly, in California, Kaiser Permanente dominates the market, as both the health system with the most discharges (13.1%) and the largest insurer (51.6%).

The figure below shows the health systems with the largest shares of total hospitals in each state, the health systems with the largest shares of total inpatient hospital discharges (all-payers) in each state, and the top three insurers in the large-group market by enrollment.