Shae-Marie Stafford-Trujillo has spent a lot of time in hospitals.

At the age of 23, she’s been diagnosed with narcolepsy, osteopenia (low bone density), an optic nerve disorder, and fluid in her brain. She also grew up with family members going from doctor to doctor for their own chronic illnesses.

Her impression of physicians wasn’t always positive. Some doctors dismissed her symptoms. Some made her family members feel their suffering didn’t matter.

But some listened. Some fought for her.

Both the negative and positive experiences fueled her desire to pursue a career in medicine.

“I have so much of a passion for patients, being a patient myself,” Stafford-Trujillo says. “I refuse to let anybody feel how I have felt and continue to feel — broken down by the system.”

She is currently enrolled in a postbaccalaureate program at Baylor College of Medicine in Houston and works in a neuroscience lab while studying for the MCAT® exam and preparing to apply to medical school next year.

But now, as the U.S. Congress considers legislation that could result in significant limits on federal student loans and change the criteria for medical residents qualifying for the federal Public Service Loan Forgiveness (PSLF) program, Stafford-Trujillo worries she won’t be able to afford to go to medical school at all.

“Most people my age have already taken out loans. [I did] to go to college, to live, for the postbaccalaureate program,” she says. Limiting federal student loan borrowing “would make medical school not an option. Period.”

The legislation working its way through Congress could limit one type of federal loan relied on by all medical student borrowers (Direct Unsubsidized loans) and eliminate another key loan program (Grad PLUS) used by over half of medical student borrowers. Other details of the legislation will impact most areas of higher education.

The proposed changes have prompted an outcry from members of the medical community, as well as opposition from the AAMC, the American Association of Colleges of Osteopathic Medicine, the American Medical Association (AMA), and dozens of other physician groups.

The groups have published statements and sent letters to Congress arguing that the changes could worsen the physician shortage, prevent people from lower-income backgrounds from pursuing medicine, and drive doctors away from lower-compensated jobs, such as those in primary care specialties and working with underserved populations.

“Every aspiring physician deserves a fair chance at a medical education — no matter their economic background. Federal student aid programs like Grad PLUS loans and Public Service Loan Forgiveness help make that possible for nearly half of all medical students,” AAMC President and CEO David J. Skorton, MD, and Chief Public Policy Officer Danielle Turnipseed, JD, MHSA, MPP, said in a statement. “Eliminating or restricting these critical programs would undermine the future physician workforce and ultimately make it harder for patients in communities nationwide to get the care they need.”

Loan caps

As part of the spending bill, known as the One Big Beautiful Bill Act, the U.S. House of Representatives passed several changes that would impact medical student borrowers starting July 1, 2026, should it become law. On June 10, the U.S. Senate Committee on Health, Education, Labor, and Pensions released a proposed bill with some differences from the House version. If it passes in the Senate, it will have to be reconciled with the House before it goes to President Donald J. Trump to be signed into law.

The House bill limits federal Direct Unsubsidized loans for students in graduate and professional programs, including medicine, to a total of $150,000. The Senate proposal sets the limit for professional programs at $200,000. Both versions eliminate Direct PLUS (Grad PLUS) loans, which were introduced in 2006 and allow graduate students to borrow up to an institution’s established cost of attendance to pay for expenses related to their studies, including living expenses.

The median amount of debt for the medical school graduate class of 2024 was $205,000. The median four-year cost of medical school attendance for the class of 2025 was $286,454 for public schools and $390,848 for private schools, according to AAMC data. About half of all medical students take out Grad PLUS loans, totaling more than $2 billion annually.

Those who would need additional funds would have to take out private loans, which can be more difficult to qualify for, have higher interest rates, and do not offer income-based repayment or loan-forgiveness options.

Aidan Hintze, MD, who will be starting his general surgery residency at AdventHealth in Orlando, Florida, this July, says that Grad PLUS loans helped him attend medical school at Penn State College of Medicine in Hershey while supporting his family.

Hintze says that, when he and his wife decided that he would attend medical school, they crunched the numbers and found that child care and transportation costs associated with his wife’s working would have offset the benefits of her salary. At the time, they had a one-year-old daughter and have since added two more girls to their family.

Aidan Hintze, MD, poses with his wife and three daughters at his medical school graduation.

Courtesy of Aidan Hintze, MD

“I ultimately ended up choosing a school that had the better financial aid package, scholarships, and cost of tuition,” Hintze says. “Grad PLUS loans opened up the opportunity for my wife to stay home. We wanted to give our kids something rock solid in a stressful time.”

Hintze says he is worried that current and future medical students will face more significant financial barriers than he did.

“I’m fairly terrified for the state of medicine. I have a brother-in-law in medical school, and thinking about him needing to take out loans next year … I don’t know how he’s going to make ends meet,” he says. “I have friends whose parents were able to pay their rent or other expenses, but I don’t want medicine to become one of those careers you can only do if you have wealthy parents.”

In fact, a 2018 AAMC study found that between a quarter and a third of all medical students came from households with an income in the top 5% in the country. More recent studies have shown modest increases in socioeconomic diversity among medical students.

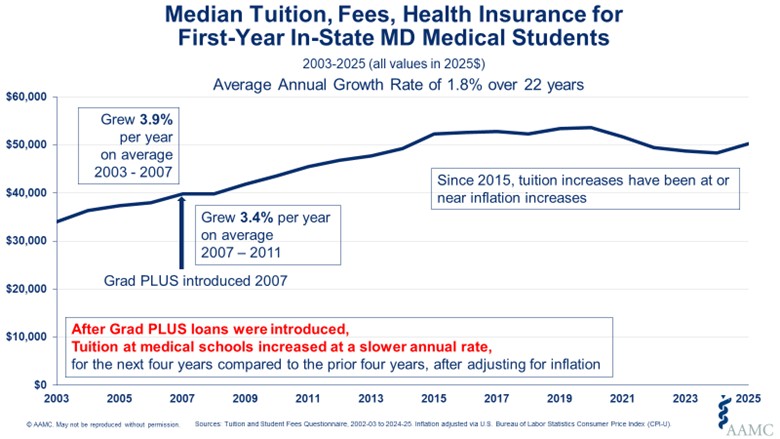

Proponents of the changes to student loans argue that the availability of Grad PLUS loans incentivizes medical schools to increase tuition, and that reducing loan options for students would force tuition reductions, thus minimizing the amount of loans students would need to complete medical school.

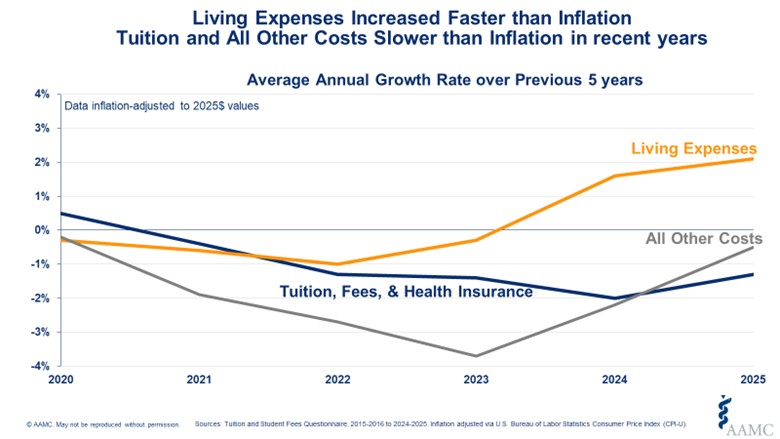

But an AAMC analysis found that, in the four years after Grad PLUS loans were introduced, the average annual growth rate for medical school tuition slowed compared with the four years before the loans were introduced, after adjusting for inflation. And since 2020, the average medical school tuition and fees have grown at a slower rate than inflation, while general living expenses increased faster than the rate of inflation.

Public Service Loan Forgiveness

Another program that could face changes in the pending legislation is PSLF, which was passed into law in 2007. Under the program, people who work full-time for a qualified employer (generally a nonprofit or government organization) and make 120 monthly payments (usually over 10 years) can have the rest of their loan balance forgiven. Since teaching hospitals are often eligible employers, many physicians who intend to work in public service jobs after residency can also count their time in residency toward their loan forgiveness. In a 2024 AAMC survey, 63% of graduating medical students indicated they planned to enter a loan-forgiveness program, and of those, 88% indicated they intended to pursue PSLF.

Both the House bill and the Senate proposal exclude time in residency from counting toward PSLF. The House bill would allow medical residents to defer loans without interest accrual for up to four years, but the Senate proposal does not include this provision.

These changes would go into effect for loans borrowed after July 1, 2026, so current residents would still be eligible under the existing guidelines.

Under current policy, students have several options for repaying loans, including income-driven plans that scale monthly payments at a percentage of a borrower’s discretionary income. One AAMC simulation of paying off $205,000 in direct federal loans shows that interest over 10 to 23 years could add anywhere from $133,000 to $250,000 to the loan, depending on the repayment plan, with those receiving PSLF paying the lowest amount. The House bill and Senate proposal also change the options for repayment for those taking out loans starting July 2026.

For Melissa Robinson, MD, a pediatrician and interim associate dean for admissions at the University of South Carolina School of Medicine Greenville, the idea that the prospective medical students she works with now may not be afforded the benefits that she reaped from PSLF is disheartening.

Courtesy of Melissa Robinson, MD

Robinson says that knowing she would be eligible for loan forgiveness helped her choose pediatrics, a specialty compensated at lower rates than many other medical specialties. She completed her residency training in 2017 and turned in the PSLF paperwork last year. Six months later, she received a letter noting that her debt balance had been forgiven.

“It’s made a huge difference. Having a path to the forgiveness really helped reduce the stress of having that debt, even before paying it off, and it really opened the door to allowing me to go to medical school wherever I wanted that best fit my needs and desires and mission in the field of medicine,” Robinson says. “It opened a whole pathway of career that I didn’t know about right when I first started medical school.”

Now, as a dean of admissions, Robinson works with incoming medical students and has heard firsthand how uncertainty around loan-forgiveness options might steer qualified applicants away from primary care fields, working in underserved communities, or even away from medicine altogether.

Leana Nápoles, MD, who is completing her pediatric residency this summer, was careful to make sure the county clinic she will work for after residency qualified her for PSLF. Before attending medical school, she worked in the Peace Corps at an HIV/AIDS clinic in Ecuador and at a research lab at the University of California San Francisco, which, along with her three years of residency, give her six years of qualification toward PSLF.

Leana Nápoles, MD, poses with her parents at her residency graduation.

Courtesy of Leana Nápoles, MD

“It gave me some nice financial support, that if I did want to do this — to work for underserved people — I’m not going to get into mounds and mounds of debt,” Nápoles says.

Now, even though the policy changes in the proposed plan wouldn't impact her, she worries that the uncertainty and future federal policy changes could still jeopardize her loan-forgiveness plans. And she’s even more worried for the medical students who would be directly impacted by any changes.

Nápoles acknowledges she came into medical school with some privilege, including that her father is a doctor and she had some support from her family when she had no income. But even with these privileges, the student debt she’s accumulated has impacted her financially. She was recently denied a small car loan due to her student debt load.

She understands how the fear of taking on debt without the promise of forgiveness might deter students from pursuing a medical specialty or practice area that is focused on underserved populations.

“PSLF is not just a policy,” Nápoles says. “It’s a lifeline that makes service-driven medicine possible.”